Content Warning: This is not a post about the manufactured housing industry. This is a post about option pricing. Readers looking for the usual crap can click here, here or here.

In the fifth and sixth seasons of The Crown, now-King Charles is played by Dominic West. This causes cognitive dissonance. Dominic West is good-looking, smart, solidly built and professionally capable, and he has strong neck muscles indicative of hybrid vigor. Charles, by contrast, is an inbred, bleating twit. Here is West, in his role as Detective McNulty, in The Wire:

And here is Charles:

I do not understand the secret sauce that makes men attractive. I don’t care much about it, because I do not have a dog in that fight – but even a straight guy like me can see that there is no comparison between these two men. Using West to portray Charles is like using an apple to denote a spark plug. A disclaimer at the beginning of each episode states that the series is fiction. Maybe that is the drag in which the producers dress their decision to use Mr. West to portray Charles. I do not buy that explanation. The series is brilliantly produced and well worth watching, but we watch it because it is true. If it weren’t, we would turn the channel to something with sex and violence, like Fauda, or Game of Thrones.[1]

Other recent sources of cognitive dissonance include the following:

- My eighteen-year-old child lingering after dinner to have a thoughtful conversation with me;

- Park residents who don’t flush baby wipes down their toilets;

- A junkie who broke into Josh’s home after Josh died and told Mike that she would leave after she stuck a needle in her arm and depressed the plunger;

- A resident who threatened to sue me and told me that he was represented by my lawyer;

- A public defender who spent months putting up frivolous Fabian defenses which caused her client to miss the final ERAP deadline;

- Residents who clean their lot and pay on time; and,

- Near-the-money option prices on the VIX.

It’s the VIX that really confuses me.

For more detail about the VIX, see here.[2] I am confused by the current behavior of June and July puts on that index. Readers who understand what is causing the phenomenon that I describe below are encouraged to enlighten me.

Option prices consist of either one or two values. In-the-money options have intrinsic value, i.e. value that the holder would recognize were she to exercise the option immediately. This is equal to the difference between the price of the underlier and the strike price. Every option – in-the-money, at-the-money and out-of-the-money – has option value.[3] This is the value of the probability-weighted outcome that the option will go (further) into the money before expiration. Inputs used in computing option value include moneyness, time to maturity, interest rates, dividends, and expected volatility. Note time to maturity as an input; option values tend to decay over time, because the amount of time prior to an option’s expiration decreases as the days and weeks pass. As the value of the input decreases, the value of the output, i.e. the option price, decreases.

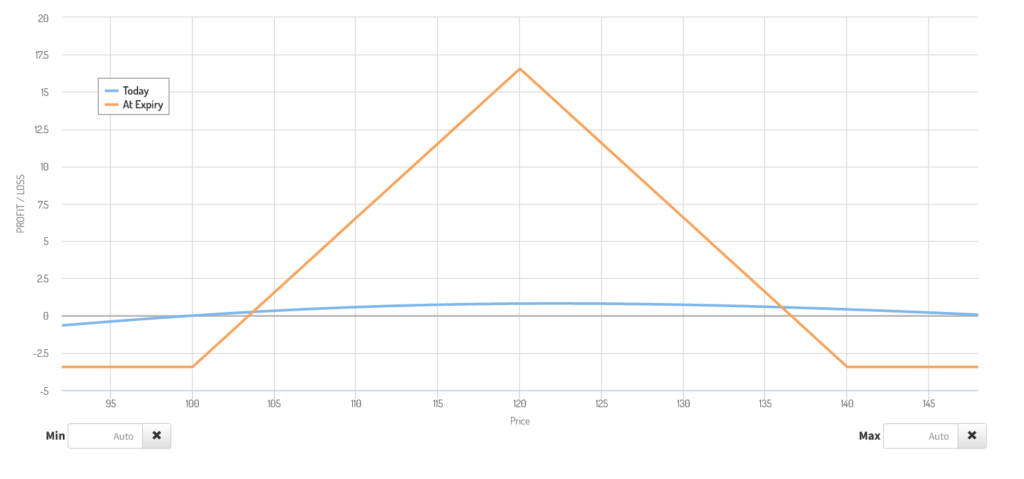

Most option positions are not one-leg buy-or-write transactions. Most consist of two or more legs. For example, a butterfly spread consists of a long position in 1x options, a short position in 2x same side but further away-from-the-money options in the same underlier and a long position in 1x yet-further-away-from-the-money same side same underlier options. Option pay-off diagrams are drawn as a graph with the price of the underlier on the X axis and the value of the position at maturity on the Y axis. The payoff diagram of a butterfly spread consisting of 1 long position in a 100 call, 2 short positions in a 120 call and 1 long position in a 140 call on ABC stock with premium values for the 100, 120 and 140 options at $12.82, $6.00 and $2.62 respectively would look like Chart 1:

Chart 1

(An oil trader, who sat next to me in Finance One, liked to talk about ‘liftin a leg’ and how his wife got angry when he told her that he was trading crack spreads. He was a thug, even though he wore a yalmuka.)

Butterfly spreads have negative vega. That means that, prior to expiration, they tend to gain value when implied volatility decreases. This is because, when implied volatility tanks, the value gained by the two short positions that form the body more than offsets the value lost by the long positions of the wings.[4]

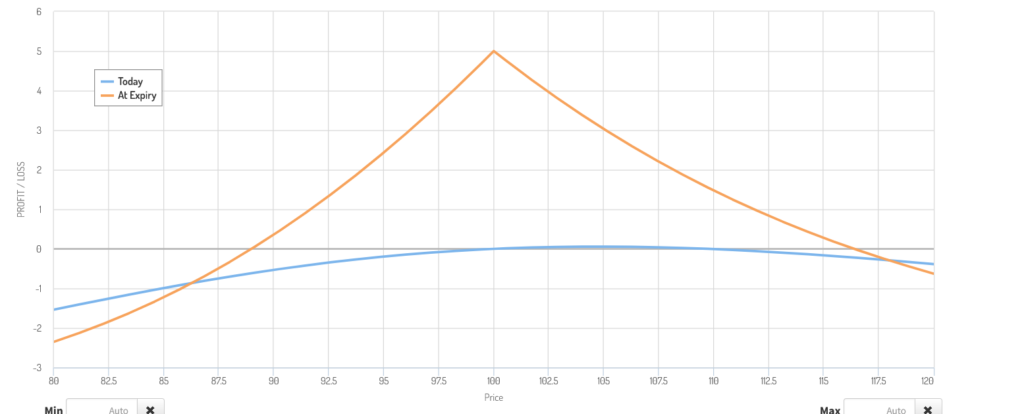

In a calendar spread, a near-month option is shorted and a longer-dated option with the same side, underlier and strike-price, is bought. If the position is held until maturity, the hope is that the near-term option will expire worthless but the longer-term option will retain enough value to more than offset the initial cost of entering into the position. Chart 2 shows the pay-off graph of a calendar spread consisting of a short position in a 100 call on ABC stock with a maturity of 183 days and a long position in a 100 call on the same stock with a maturity of 365 days. Premium for the short-dated option is $8.92 and premium for the longer-dated option is $12.82:

Chart 2

Readers will notice that the pay-off graph for a calendar spread looks kind of like that for a butterfly.[5] In both cases, the profitable area is a tent that peaks at the two short positions in the case of the butterfly, or at the common strike price in the case of the calendar spread, and in both cases the risk in the trade (i.e., the area below the ‘0’ line on the Y axis) is limited. Total risk in each trade is the amount paid to enter into the trade. In the case of a butterfly, the cost of entering into the trade is the difference between the cost of buying the wings and the premium collected by selling the body. In the case of a calendar spread, the cost is the difference in price between the longer-dated option and the shorter-dated option. Because option value decays as time passes, longer-dated options cost more than short-dated options. That is why it costs money to enter into a calendar spread. The thing you buy costs more than the thing you sell.[6]

If you could enter into a calendar spread for free, your risk should be zero. Risk-free gain is arbitrage. The market abhors arbitrage the way nature abhors a vacuum. Traders, by contrast, love it.

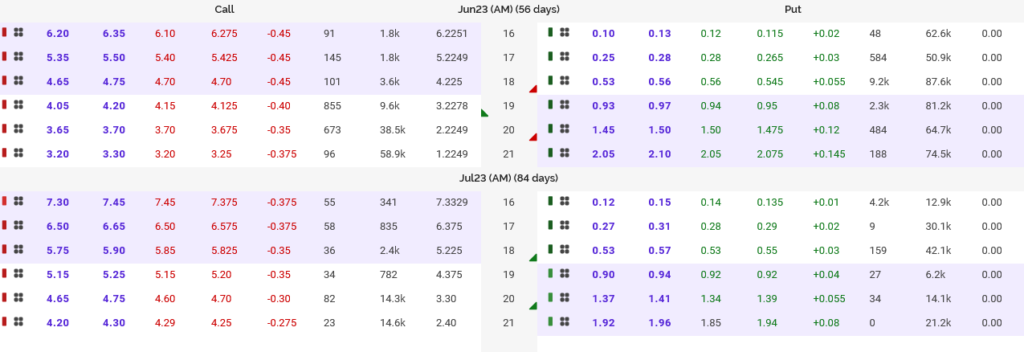

Table 1 shows an option chain for the June and July expirations of VIX options. This is the source of my confusion. Either something is off, or I do not understand something:

Table 1

Puts are on the right, calls are on the left. Strike prices from 16 to 21 are shown. The underlier is the VIX. June expirations (56 days from today) are displayed on the top. July expirations (84 days out) are below. The farther-out puts are cheaper than the near-month puts. For example, the June 19 put is bid at .93 and offered at .97, and the July 19 put is bid at .90 and offered at .94. The farther into-the-money you go, the more pronounced the pattern becomes. That means that, if you get decent execution, you can enter into a calendar spread on the VIX for free, or maybe even collect a small credit to do it. That is risk-free gain. That is crazy. That is like having Dominic West play King Charles.

I do not know what to make of this. A skew in strike prices would be understandable in certain VIX-correlated products. As discussed previously, levered VIX ETFs gain exposure to the index by entering into futures on the VIX. These futures suffer from severe contango, which causes the ETFs to lose value over time. That is reflected in the prices of longer-dated options on those products – but that is not relevant here. The options we are discussing here reference the cash VIX index. To my knowledge, that index does not suffer from contango-like drift. It has the same value for each expiration month.

What is going on? Is something at work that I do not understand, or is money on the table? Readers who know are encouraged to contact me before they bid up the price and ruin the opportunity for the rest of us.

We will be back with the usual crap next week. A resident in the northern New York park who we have been trying to get rid of for two years, who took a baseball bat to his wife last month, is angry because he has been served with a warrant. We are ordering three new homes from Clayton and will pour pads to put them on. The septic aerators seem to help keep the tanks clear. I have finally learned how to spell ‘aerator’. Watch this space.

[1] I am not sure why the producers did not hire a nebbish to play Charles. Either they thought that viewers would prefer to spend 20+ hours looking at someone who looks like Dominic West to looking at the real thing, or no actor nebbishy enough to play Charles convincingly made it out the door to the audition.

[2] If you want to educate yourself about options generally, I suggest Tastylive. People who want to step into the ring themselves should check out tastytrade.com , an excellent brokerage for active options traders run by the people who operate Tastylive

[3] Far in- and out-of-the-money options have very little option value. At the periphery, options become lottery tickets.

[4] The legislative history to Internal Revenue code 1256 indicates that, when the provision was debated in committee in 1981, Tip O’Neill said that he had previously thought that a butterfly spread was a sexual practice engaged in by members of the court in the Ming Dynasty. That would not have gone over, post C-SPAN.

[5] Although calendars and butterflies are similar, they are not identical. The ‘tent’ at pay-off in a calendar is curved rather than straight because, at pay-off, the long-dated option will still be outstanding. Because that option will have some time left to maturity, it will have some option value remaining, and changes in option value, unlike those in intrinsic value, are not linear. Second, calendar spreads have positive vega. This means that, unlike butterflies, they tend to gain value when implied volatility increases, because the gain in value in the long position more than offsets the loss of value in the short position when implied volatility climbs.

[6] It is possible to enter into a reverse calendar spread, in which the short-dated option is purchased and the long-dated option is sold. This can be profitable with far out-of-the-money options. In these cases, the near-dated option is almost worthless, but the far-dated option still has some time value left. The play is to buy the near-dated option for a nominal sum and to benefit from time-decay of the further-dated option.