In the early eighties, the U.S. government didn’t know what to do about bearer bonds. The government hated them because they are a tool for tax evasion. American corporations that donated to political campaigns, by contrast, liked them because they are a good way of raising capital. So in 1982, Congress split the difference by passing the Tax Equity and Fiscal Responsibility Act of 1982, or TEFRA. Under the applicable sections of TEFRA, US-resident taxpayers can issue bearer bonds, so long as certain procedures are met to ensure that they are only offered to foreigners at original issue. We didn’t eliminate tax evasion, you see. We just exported it.

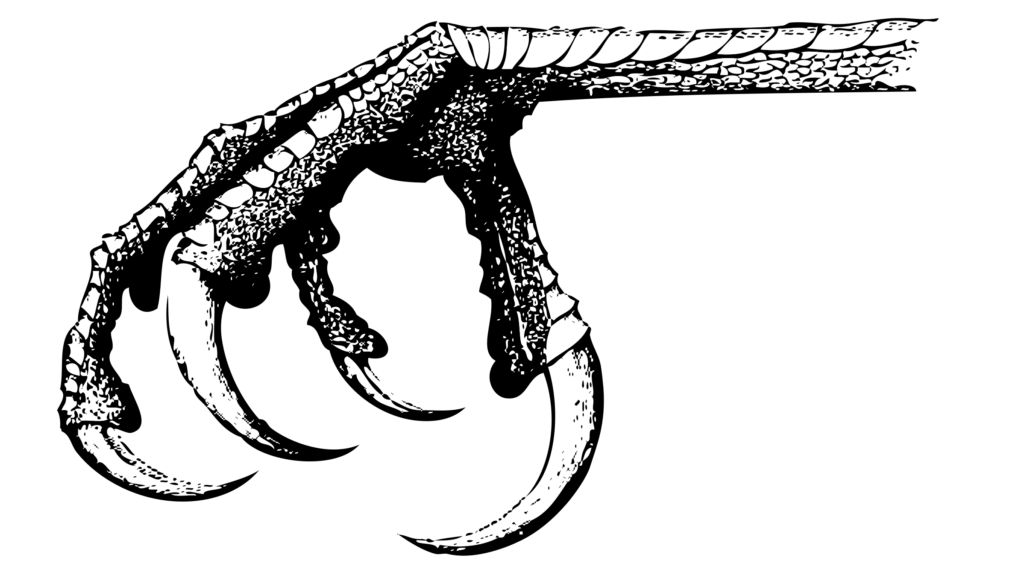

Two sections of the act (‘TEFRA C’ and ‘TEFRA D’) provide market participants two different ways to comply with the TEFRA restrictions. I don’t remember much about either, but I do recall that both included provisions regarding communications between brokers and investors during the initial post-issuance period, and one or both included some language that had to be printed in the prospectus and in the bond itself. In the body of the legend and in some of the legislative history, the term ‘talon’ appears, next to the term ‘coupon’. More than once, at three in the morning in an office in a high-rise building in midtown Manhattan, poring over a bond disclosure in my suspenders and loosened yellow tie, my jacket on the door, my free take-out dinner long-since digested and my car service waiting for me downstairs, I thought, Why did Packwood and Tip O’Neill insert language about large claws of the type one finds on birds of prey into this legislation, and what were they smoking?

After the Internet was invented, I googled ‘talon – bond’, and learned that a talon is a printed form attached to a bearer bond that enables the holder to apply for a new sheet of coupons once the existing coupons have been used up. A coupon is a piece of paper that the bearer can present to the issuer of the bond in exchange for an interest payment; a talon is a piece of paper the bearer can present to the issuer in exchange for coupons.[1]

Before I had access to the Internet, I thought that an allonge was an arrangement entered into in pre-revolutionary France between a member of the nobility, his wife, his daughter, and a member of the Third Estate chosen for his shoe size. I thought that it had its roots in late Antiquity and the early Middle Ages, when dukes and earls left their families to go fight the Crusades. I thought that the custom was enriched by Normans returning to their homes from the Middle East, bringing back practices that they had learned from Turks, Arabs and Byzantine Greeks – and their women – and that it had acquired a stylized and complex set of rituals that were described in detail by shocked Scottish visitors. I thought that the practice went underground with the Terror, but that Robespierre and Bonaparte were secret practitioners, it came back into the open with the re-establishment of the monarchy, that Dreyfusards and anti-Dreyfusards put aside their differences when they met, naked, en allongeant and that middle-class people enter into arrangements á l’allonge in the suburbs of Paris, Lyon and Strasbourg to this day. I was even thinking of taking a trip to France to try it out.

I was disappointed to learn that an allonge is a loan modification.

I have written previously about my allonge with the lady loan officer at the large regional bank headquartered in central New York. The note on my park in northern New York is five years old this month. On May 1, the interest rate on that note will re-set. Since rates have risen since 2018, my monthly payment will go up. When I asked the loan officer if she could help me with this problem, she suggested an allonge, whereby the amortization term will be stretched five years beyond its original term. I said, ‘sure’. She sent documents. I sent them back when I noticed that the draft allonge would re-set the prepayment penalty schedule. She sent me an updated draft, without the prepayment re-set. I congratulated myself, printed out the documents, and read them.

They screwed it up again.

The original note states that the amortization period will be twenty-five years from the date of the issuance of the note, and that payments are to be made on a level-payment basis over that time with no balloon at the end. Here’s what the operative language in the new draft allonge said:

Commencing on June 1, 2023 (the first day of the month following the determination of

the new interest rate) and every five (5) years thereafter on June 1st, the monthly payments will

be adjusted in order that the unpaid principal and accrued interest shall be paid in full over an

amortized period of twenty-five (25) years from the date of this Mortgage Note in substantially

equal monthly payments. All unpaid principal and interest, if any, shall be due and payable on

the Maturity Date.

In other words, the amortization term would be adjusted to the exact same term as it was in the original note. Like the map in the Borges story that is as big as the country it depicts, the amended amortization term would be the same as the original amortization term. I wrote back to the loan officer and said that I thought that what the lawyers meant to say was that unpaid principal and accrued interest would be paid in full over an amortized period of thirty (30) years from the date of the Mortgage Note, or twenty-five (25) years from the date of the Allonge. She responded with corrected documents within two hours. I immediately signed the documents and sent them back.

In addition to the allonge, the banks asked me to sign a statement of beneficial ownership, stating that I was the sole owner of the borrower, and a re-confirmation of the recourse guarantee. They also attached an invoice for the fee of the lawyer who drafted the allonge. It is a small fee and it would be churlish of me to contest it, but in a just world, my fee for legal services expended in cleaning up the documents that the banks’ attorney screwed up would more than offset the fee incurred by the bank’s attorney in drafting those documents. But this is not a just world. That is why people hate lawyers.

[1] Yogi Berra once brandished a check made out ‘to bearer’ and said, ‘See – they can’t even spell my name right’. But he didn’t say many of the things that he said.

It’s a good thing you are a lawyer. Think of the poor suckers who might not be able to read the fine print as finely as you. Yikes ?!

That’s why people dislike me.

Désolé de te décevoir, John, mais on ne pratique pas l’allonge dans les faubourgs de Strasbourg, qui est une cité antique et honorable. A Paris, je ne sais pas, peut-être dans les bureaux de DSK.

Sinon, je trouve dans le Vocabulaire Juridique de Gérard Cornu (sic) : « Allonge : Feuille de papier attachée à un effet de commerce pour recevoir les endossements qui ne peuvent plus, à raison de leur nombre, être portés sur l’effet lui-même. » Bref, ce que Proust, qui s’y connaissait, appelait une « paperolle ».

Ah! M. Le Professeur – vous me cassez les reins!